2024 State of Edtech Fundraising | Newsletter #71

We asked 20+ edtech investors about the state of fundraising in edtech. Here's what they told us.

Hi there! Alberto and Michael from Transcend here.

The Transcend Newsletter explores the intersection of the future of education and the future work, and the founders building it around the world.

We welcome 165 new readers to the newsletter since our last post. If you love reading about the future of education and work, hit the ❤️ button and share it with your friends!

Last year we set out to understand how edtech investors gauged the state of the market, and we published the first State of Edtech Fundraising newsletter. It was a hit, so we are back for more!

We have surveyed and interviewed partners and investors at the biggest edtech funds, as well as some generalist investors investing in the space. In today’s piece, you’ll read their current analysis of the market, predictions for next year, and advice for founders.

Welcome once again to the 2024 State of Edtech Fundraising!

Where we are at today

The last year and a half hasn’t been fun for any founder fundraising.

We all know the story at this point: after thirteen years of zero (or near-zero) interest rates across most economies, skyrocketing inflation and global conflict forced central banks to raise interest rates drastically.

This has made things very tough for startups.

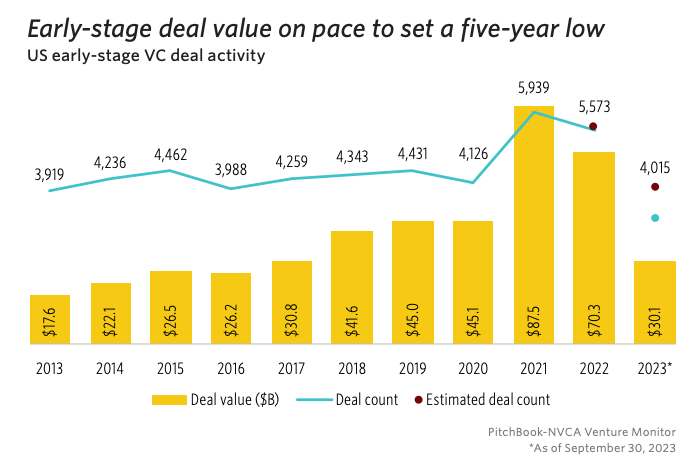

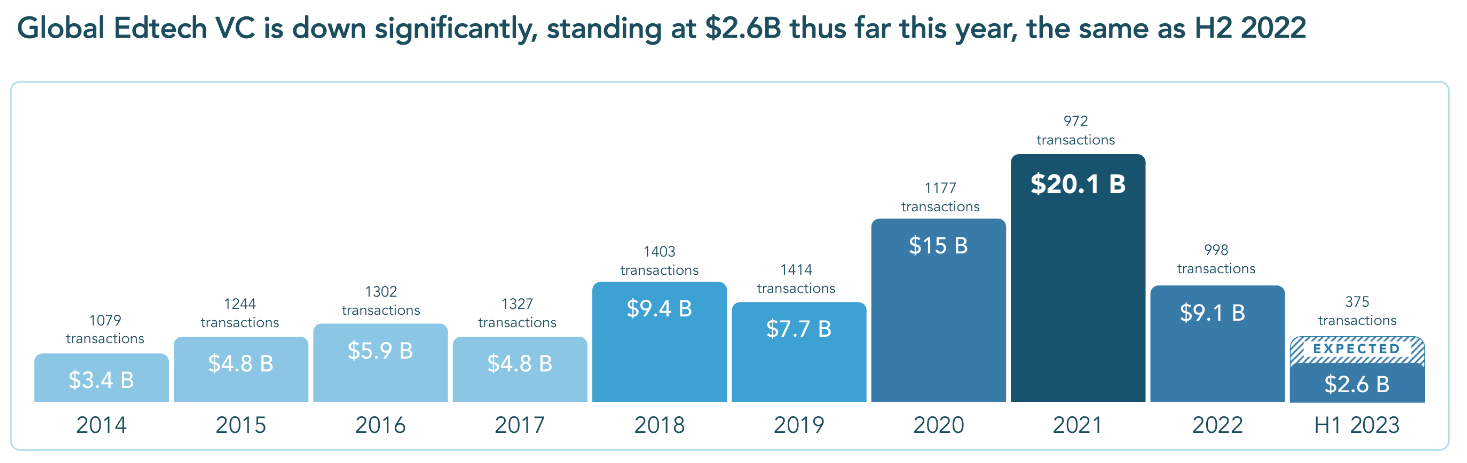

On one hand, it has driven up the cost of capital, which means there is less M&A opportunities than before, which decreased investment. But there is also less funding available for startups: Limited Partners (or LPs) who invest in VC funds now have safer alternatives to invest in (such as government or corporate bonds), which means they allocate less of their $ to VC funds, which eventually leads to less $ for startups. Globally, early-stage investing this year amounts to almost a third of 2021’s, representing the worst year since 2017.

Edtech has been hit particularly hard, with a big dip from 2021 ($20B vs $4B expected for 2023). However, if you isolate the Chinese government’s crackdown on edtech that killed all China funding since 2019, then the current funding numbers are actually fairly similar to pre-COVID funding levels.

We asked investors to zoom into the trends they are seeing, so let’s dive in!

5 Fundraising Themes from 2023

Valuations and check sizes have continued to decrease: among the investors we surveyed, 56% reported investing at lower valuations than last year.

Last year, that figure was 73%, so it may be a sign that valuations are settling down. However, there are some signs of optimism in sectors like K-12 or AI.

Let’s explore these 5 themes:

1. The “First-check Gap”

The bar has been raised for anyone raising a pre-seed: the revenue benchmarks that investors request are much more demanding now, whereas in past years, a good idea and team may be enough to put together a pre-seed round. Miriam, from Brass Ring Impact describes this challenge for founders:

“Several companies have either closed rounds at a lower amount than was their initial goal, have experienced 2X the expected time to close their rounds, and/or have settled for lower valuations”

Additionally, many edtech VCs raised new funds during COVID, with a handful of funds entering the hundreds of millions of AUM (Assets Under Management). Once your fund manages $500M, a $200k check into a pre-seed round simply isn’t enough: funds are looking for bigger investment opportunities and equity stakes, so they can return their fund with a few big winners.

This has created a growing “first-check gap” for founders raising their first round of funding and struggle to raise from institutional investors, even if there are more investment options at the seed and Series A stages.

Instead, angel investors are taking on the role of pre-seed investors. Many great founders we work with have raised pre-seeds exclusively from angel investors. Jessica Millstone describes this gap:

“For those who are actively fundraising, a true pre-seed round (at/around $1mm) seem unrealistic and more is being accomplished with a few angel checks”

This comes with new challenges, as angels are hard to find and reach, and can’t always follow-on for the next round. But it’s the reality: a few small funds and angel investors are taking on the role of first-check investors for early-stage startups.

2. Early-stage is on the move; Late-stage is dead

During 2020-21 years, there were more than 60 rounds of $100M or more. This year, there hasn’t been a single one. Zero.

Later-stage investing is dead right now. Funds have been very focused on bridge rounds for their existing portfolio, and investing in new companies at the seed or Series A stages.

“There have been very few Series B+ rounds in the last 18 months or so. I'm optimistic that things will pickup for growth and later stage companies in 2024.”

- Graham Forman

Bridge rounds were also a trend in 2022 and 2023. Many funds saw their portfolio companies struggle to raise, and had to step in to stop the bleeding. As Yigal from JFF Ventures put it: “Rounds take longer to come together, and as a result, companies are opting to raise extension rounds to extend runway”

But early-stage investing was more alive, and AI played a big role in this: 56% of surveyed investors mentioned AI as the main trend they are following this year. However, while a lot of startups used the AI buzzword to raise while only having a few AI features, there are still few AI-first companies, according to Mario from Emerge.

“The use of generative AI has been the main trend. It has become a very crowded space”

3. It’s K-12’s moment!

K-12 is going through a big transformation. All the attention that COVID put on the outdated state of K-12, plus all the ESSER funds that flooded US schools and districts brought a lot of attention from founders to build in the space.

In 2024, ESSER funds will dry up, and founders are focusing on using AI and other technologies to solve fundamental problems in K-12, such as early literacy, AI educators copilots, teacher recruitment, mental health, and more. These problems aren’t ESSER-funded “nice to haves”, but real problems that schools have experienced for decades.

Graham Forman, who’s one of the leading K-12 investors at Edovate, summarized it best:

“I invest at the pre seed and seed stages in B2B K12. For me, the last 15 months or so have been the busiest period of investing since I started doing this full-time about 10 years ago. I'm seeing a lot of aligned founders tackling high priority problems faced by K12 schools and districts.”

Many startups will struggle with the transition as ESSER funds come to an end next year, but those who manage to solve real problems for schools and districts will remain strong.

4. Edtech isn’t all about VC

We’ve written before about how edtech isn’t just about VC, it’s a sector with great “funding model diversity”: historically, we have seen education organizations thrive under venture-backed, nonprofit or bootstrapped models, and more recently have seen the rise of patient capital and corporate partnerships as viable models for startups in the space.

However, the narrative around startup funding is dominated by venture capital. Many non-venture-scale startups are raising from VC funds – Katelyn Donnelly from Avalanche VC argues that while this has always happened, “now VCs are most discerning on business models and moats they invest in”.

A few models with proven ROI for VC funds will receive funding, and all others will have to find their own “funding-market fit”. This will lead to innovations in funding mechanisms and business models, as Jessica Millstone suggests:

“I’m really excited about the potential for mixed capital (strategic/philanthropic/venture capital coming together to fund edtech startups) and what the potential business models that will emerge to take advantage of this more patient capital”

5 Investment Themes for 2024

We asked investors what themes they were most enthusiastic to invest in this coming year, and here are their answers.

Theme #1: Talent

An overarching theme for 2024 is the focus on talent: training, placement and management.

Funds like JFF Ventures, Brighteye Ventures or FullCircle are interested in investing in workforce development and staffing solutions for high-demand roles, like training and placement for the green or the care economies, and vertically integrated solutions in key industries.

Charter Schools Growth Fund and Edovate Capital are focused on K-12 talent bottlenecks. Here’s how Ian from Charter Schools Growth Fund defines it:

“Talent is the most significant expense for schools and will be a top 3 priority for the foreseeable future”

This talent theme isn’t limited to just hiring, but also growing your talent at the company, as Virginie from FullCircle framed it:

“Giving everyone more agency, ownership and pride in their work is a key driver of economic prosperity and mobility!”

Theme #2: Health & Learning

There’s traditionally been a big “wall” between the health and education spaces*.* But those lines are thankfully getting blurrier, and investors are excited to explore that intersection: from mental health, to personal health to pediatric behavioral and developmental health.

From a business model point of view, the role of government agencies and insurance companies as buyers adds more depth to the market potential.

Funds like Reach Capital, Brighteye, GSV and Rethink Education expressed interest in these spaces.

Theme #3: Personalizing learning

One of the big, hairy problems in education is how costly it is to personalize a learning experience for a single student. While it’s the most effective, it usually requires an instructor to spend time personalizing the instruction. One high level theme that many investors mentioned is using AI, other technologies or communities of peers to drive down the cost of personalized learning experiences.

GSV, Brighteye Ventures, Reach Capital and Ruthless for Good expressed interest in this thesis, though it has implications for almost every other theme.

Theme #4: Evidence-based investing

One of the main transformations edtech is going through is how evidence-based it is becoming: from customers (like schools or districts) requesting proof of impact for companies before approving their purchase, to VCs asking for impact metrics (so they can incorporate them into their Impact Reports) and even LPs requesting evidence-based investing in their funds.

Ben Kornell put it concisely – most funds are looking to invest in companies that “demonstrate real impact on learners/users”, not just clever ideas!

Theme #5: Optimism for 2024?

2023 has been another year of corrections and down-rounds, but there’s an underlying sense of optimism for next year. 95% of investors said the quality of startups they are seeing is higher or similar than in previous years, up 10% from last year.

We also learned that 65% of the investors surveyed will be raising a new fund in 2024, which will bring new opportunities for startups to receive investment.

That’s all from us today – we’d love to hear what you think, so please leave a comment with some of your learnings and takeaways!

Want to learn more from some of the investors we talked to?

Join us for our Open Discussion on the 2024 State of Edtech Fundraising on Jan 10!

We will be joined by leading edtech investors Jessica Millstone (Copper Wire Ventures) and Graham Forman (Edovate Capital) to join us for an hour-long discussion where we answer questions like

➡ Should we expect the funding winter continue through next year?

➡ What are the latest trends among edtech investors?

➡ What do early startup valuations look like? And,

➡ What can early-stage founders building in this space expect when raising funds in 2024?

We will be announcing our panel speakers in the coming days.

If you wish to join us for this session, RSVP here.

Huge thanks to all the investors who participated in the 2024 Edtech Fundraising survey: Yigal Kerszenbaum (JFF Ventures), Benoit Wirz (Brighteye Ventures), Deborah Quazzo (GSV Ventures), Graham Forman (Edovate Capital), Ben Kornell (Common Sense Growth Fund), Miriam Altman-Reyes (Brass Ring Impact), Ian Connell (Charter School Growth Fund), Jessica Millstone (Copper Wire Ventures), Victor Hu (Lumos Capital Group), Ebony Brown & Monique Malcolm-Hay (Rethink Education), Michael Ladipo (Ruthless for Good Fund), Jason Young (Long Term Impact), Hester Spiegel (Epic Angels), James Kim & Chian Gong (Reach Capital), Eric Lavin & Katelyn Donnelly (Avalanche VC), Emily Foote (Osage Venture Partners), Virginie Raphael (FullCircle), Mario Barosevcic (Emerge Education), Enrico Poli (Zanichelli Venture) and all the investors who contributed anonymously to the survey!

The Roundup ☀️

🙌 29 founders from our latest cohort (TF12) completed their Transcend Fellowship experience last week. Learn more here.

🌏 4 Transcend Fellows made it to Holon IQ’s most promising 50 edtech startups in Southeast Asia. Learn more here.

💻 Sonny Li and Codédex (TF11), raise $750K in pre seed funding to serve Gen Z students through their learn-to-code platform. Learn more here.

Thank you for reading!

Did you enjoy reading this piece?

Hit the ❤️ button to help us reach more awesome people like you!

Good post stating important facts.

Entrepreneurs also need to stay focused on financial health - personal and for their initiative. VC fundraising is only one source of growth capital. Internal accruals that come from recurring revenues from customers is probably one of the most sound ways to fund growth. I am doing this myself as someone building an advisory business.

Akhil Kishore

GIA ADVISORS